Human nature has us convinced we’re more risk-tolerant than we actually are.

While it’s easy to say you’re a risk-taker when it comes to quite literally putting your money where your mouth is the story is often a little different.

Even if you think you could watch 50%+ of the value drop from your portfolio without breaking into a cold sweat, it’s still a good idea to know what risk level you’re getting yourself into when deciding between investment options.

So how does the potential risk of website investing compare to other popular investment strategies? Well, with this guide to risk, you’re about to find out.

But first…

It goes without saying (but just in case): the following article does not constitute investment advice and should not be taken as such.

With that out the way, let’s take a look at your options before moving on to their associated risks.

Types of Investments

This is by no means an exhaustive list, but it does cover the most popular investment options available. If you feel that we’ve missed one, let us know in the comments below.

Cash Savings

We’ll look at why this might not be the safe choice many think it is later on, but it should be stated that it is still advisable to keep some cash on hand at all times.

Before investing in any of the following assets, build up and maintain easy access to money that covers 3-6 months’ worth of expenses.

Having an emergency fund ensures you’re not forced to sell a stock at a bad time and covers you while you’re unloading some of the more illiquid investments such as property and to an extent, websites.

Stocks and Bonds

Although a wide-reaching term, for this article we’ll use ‘stock’ as an umbrella term to include individual shares (eg. in Apple, Facebook, etc), ETFs, Mutual Funds, Index Funds, and Commodities (eg. precious metals). It will make comparison easier and keep this article under 10,000 words!

For the same reasons, the term ‘bond’ will include the three main types under the same umbrella:

- Treasury/Government

- Municipality (US state and local government)

- Corporate

Cryptocurrencies

Supposedly the hottest new investment, cryptocurrency (or crypto) is a decentralized and encrypted digital money based on blockchain technology.

Don’t worry, to gain value from our risk comparison to website investing you don’t need to fully understand how it works. In fact, many who have made money via crypto don’t understand it themselves which is one of the reasons it’s classed as a high-risk investment.

Entrepreneurial Endeavours (Starting Your Own Business)

Although website investing is considered an entrepreneurial activity, as you own the site and have control over it, we’re going to dedicate a separate section to starting your own business. It carries a different set of risks that are worth outlining independently.

Website Investing

When we talk about the term website investing we’re referring to buying/selling websites solely to earn income. Building your own site and flipping it for profit, or buying a pre-existing site and operating it both fall under this category.

However, as we’re looking at website investing as a passive income source, we’re discounting sites such as eCommerce stores where you would need to take over the day-to-day order handling, etc for the business.

In other words, for this article website investments are content sites and the like that make money through affiliate marketing and display advertising. They require minimal upkeep and earn revenue through page traffic and link clicks.

Property Investments

For some, property investment simply means owning your own home, for others, it’s having a portfolio of rental properties (commercial or residential). Either way, the risks remain largely the same so we won’t differentiate between the two when analyzing this asset class.

To save the best till last, we’ll tackle our list of risks alphabetically. First up…

To Bond or Not To Bond

Terrible jokes aside, bonds have historically been a popular investment option to hedge against stock volatility.

Many stock-market investors recommend rebalancing portfolios to hold more bonds as you near retirement as they’re considered a lower-risk option and typically generate a better return than cash savings.

But as with most investments, the lower the risk the lower the reward.

By investing in bonds you are effectively loaning the institution money to pay off debt or fund new projects. In return, you receive regular interest payments (or coupons) on the total value of the bond plus the initial investment amount back at the end of the term.

Bonds with longer maturity tend to offer higher returns but carry higher risk, particularly if purchased from private companies. The biggest risk to a bond investment is the institution you purchased it from defaulting on the payment. While it’s highly unlikely the US government will go broke before your bond matures, a private company looking to raise finance might.

As an uninsured investment, there’s no way to recoup your losses in the event a business goes bust, unlike the FDIC protection on cash savings of up to $250,000. Depending on who you’re buying the bond from, you could be opening yourself up to more risk.

Your money is generally stuck in bonds until the end of the term so liquidity becomes an issue. It is possible to sell your bond to someone else before it matures but you often have to pay a commission on the sale and if interest rates have risen since you purchased, you risk being forced to sell at a discount to make the sale.

Analysis: Low risk, modest reward (dependent on the bond issuer)

Risks of Cash Investing

Many argue over whether holding cash really classes as an investment since you’re not doing anything with it. However, the inherent inactivity of cash is what makes it a problem.

They say that money makes money but how true that is, depends on where that money is.

Compared to other forms of investing:

- Cash offers very few growth opportunities. We’re currently experiencing a period of low-interest rates with savings accounts offering between 0.01% and 1% interest on balances. There are a few exceptions, but they usually require you to lock your money away for a fixed period of up to 5 years, thus removing the benefit of holding cash in the first place.

- Inflation devalues money over time so holding too much of it could end up costing you.

- Savings held as cash for 5-10 years are expected to lose somewhere between 5-15% of their value. Imagine then what you’d be left with if you just put the remainder of your paycheck each month into a savings account and never did anything with it — suddenly that retirement fund is looking a lot smaller than you thought.

- Another risk you face with cash investing is the opportunity cost associated with it.

By keeping it in a low-interest savings account, not only are you potentially losing money, but you’re also missing out on the opportunity for it to make money via other investments through regular income or the power of compounding.

Analysis: Low risk, low reward

Crypto, the Cashcow Investment

Well, perhaps not. While it is true cryptocurrency has made some people very wealthy, it has also lost a lot of people a lot of money.

Take a look at why we say it’s an extremely volatile asset:

- Crypto is vulnerable to market manipulation.

- It is a largely unregulated investment class and the potential for future restrictions imposed by governments and banks pose a significant risk to how and when you can hold/use it.

- Not stable enough to become a useful currency. Spend even a short amount of time in the crypto community and you’ll come across the story of the $200 million pizza.

It goes a little something like this…

In 2010 a man ordered two large pizzas from Papa Johns, paying the $30 bill with 10,000 bitcoins. At the time, these traded for around $0.003. Fast forward a decade later and the first cryptocurrency’s value has exploded, making the 10,000 bitcoins worth over $190 million. Let’s hope they at least threw in some free dips for him!

- Another major risk to investing in cryptocurrency is hacking. The coins must be ‘mined’ and stored in a ‘personal wallet’ or vault which leads them vulnerable to cyber theft.

- Since the currency is 100% technology-based, there’s no physical collateral to back it up unlike with other forms of currency or investments. Once it’s gone, there’s nothing to prove you had it in the first place.

As it sees wild growth periods some see crypto as a short-term investment, buying into the newer coins that enter the market advertised as “the next big thing in crypto” and treating it as a get-rich-quick scheme. However, this opens them up to a greater potential for loss, especially when prices have been pumped significantly.

There is a stronger argument for holding the top 5-10 currencies over the long term (HODL) as a portfolio diversifier and allowing the price appreciation to occur naturally for a safer return.

As cash left in a savings account is offering very little, if any growth, many investors are taking their chances and dabbling in the world of cryptocurrency investment for a chance at better returns.

As institutional investors flood into the market it remains to be seen what will happen to the price, however one risk regardless is the withdrawal process. In many cases it can take months to withdraw your money, leaving you vulnerable to a price slump in the meantime halving your assets.

Assuming you manage to overcome the FX issues and high minimum withdrawal rates, often depositing the sum into your bank account triggers fraud warnings that freeze your account.

Given that there is very limited ‘real-world’ use for it, financial institutions are wary about cryptocurrency, as are large portions of the investing community.

Analysis: High risk (depending on how you view crypto as a whole), high reward as part of a long-term, portfolio diversification strategy — future uncertain

Entrepreneurial Risks

9 out of 10 start-ups fail. Those are tough odds to beat.

Many see starting their own business as a way of investing in themselves. You don’t have to answer to anyone, get to do what you love, take holiday whenever you please — it all sounds pretty idyllic.

The reality is though that established markets are incredibly hard to break into:

- It takes a lot of capital, a lot of time, and a lot of hard work to make a business successful and maintain it.

- Markets move fast so to keep up you need to constantly innovate and without the expert knowledge yourself you risk spending too much revenue outsourcing.

- It’s very much an active investment. You can’t just sit back and let a direct debit feed your stock portfolio or a website generate ad revenue.

For those willing to put the time in it can be extremely rewarding, but, as many view investments as a way of making their money work harder so they don’t have to, it’s not for everyone.

Analysis: High risk, high reward (for those prepared to do the work)

Real Estate = Payment

Arguably the most expensive investment you can make (at least in one go), real estate is one of the more illiquid assets there is. Not to mention the ongoing costs it occurs:

- Mortgage

- Maintenance costs

- Home insurance

- Bills

- Utilities / Landlord insurance

- Legal fees (and stamp duty for UK investors)

Also, the market fluctuates and locations fall in and out of favor over time so your capital is not guaranteed.

While many see a rental property as a good investment thanks to the regular income it provides, having more than one can quickly cause your portfolio to become unbalanced. It’s a classic example of putting all your eggs in one basket.

With the potential for vacant periods where there’s no money coming in, fire, theft, and flood risks, and the fact that you can’t shift it quickly if you want the money out, property can be a high-risk investment. Still, it’s one many aspire to own.

Analysis: Moderate risk, moderate reward (but capital intensive)

Are Stocks Still Popular?

Visit any online investment platform and you’ll see a message very similar to the following statement.

“The value of investments fluctuates over time and you may get back less than you put in — past performance is not an indicator of future results.”

Well, fluctuates is probably an understatement most years.

While it’s certainly true that up to this point the stock market has always trended upwards, there have certainly been some wild swings and downturns along the way. The most recent being the March 2020 slump as the world reacted to COVID and the 2008 financial crash.

If you’re going to invest in stocks you need to have the nerve to keep holding even if the price plummets and know when to dump losing stocks. The idea that you can time the market is a myth, but one many spend time trying to prove.

There is undoubtedly success to be had picking individual stocks if you can find a winner but it carries a lot of risks.

Without sounding defeatist, there are a lot of losers out there — not every IPO will be the next Amazon or Shopify.

If you’re going to invest in individual stocks you need to be prepared to sacrifice a lot of time researching and take the risk that not all of your predictions will pan out. If it were easy, the world would be full of Warren Buffets. Alas, it is not.

Certain markets move faster than others and if you’re investing in individual stocks you run the risk of the market moving on the next best thing leaving your investment behind. Does anyone remember Myspace?

For a “safer” stock investment option, people who want more concrete results and none of the hassle of individual investing choose index funds that track an entire market, eg. the S&P 500.

Index funds can mitigate the risk of investing in stocks as you have a wider exposure.

Say you’d invested in Vanguard’s S&P 500 index fund VOO and tomorrow number 1 placed Apple mysteriously goes bust and crashes out of the US market. Well, had you owned individual Apple stocks, there goes all your money. However, by owning VOO, Amazon moves up the list, another company becomes the now vacant 500. spot and you’re really no worse off in the long term.

Depending on your age, stocks can be riskier as you don’t have the same time to ride out the ups and downs, regardless of whether you’ve gone individual or index.

If you were hoping to use the gains from your investments to fund a major purchase, it needs to be at least 5 years out to give you a better chance of coming out on top and reduce the risk of finishing with less than you started with.

Analysis: High risk, high reward on individual stocks // moderate risk, high reward on indexes/funds (over the long-term with compounding, assuming you avoid expensive management fees)

Website Investing

Buying a pre-existing website allows you to become an entrepreneur without dealing with the associated risks of starting your own business. But that’s not to say website investing comes without any risk, although a lot of them can be mitigated with thorough due diligence.

Sites that have an unhealthy backlink profile, suspicious traffic sources, or limited keyword targeting pose a high risk to buyers. A Google penalty or page deindexing could see traffic, and subsequently, revenue, plummet overnight.

While these pose potential major risks, they should come up as part of your due diligence process before investing.

At Investors Club we offer our members the most detailed due diligence reports in the industry so you can see exactly what you’d be getting from your investment.

If you’re interested, we’ve written a little more about our process here.

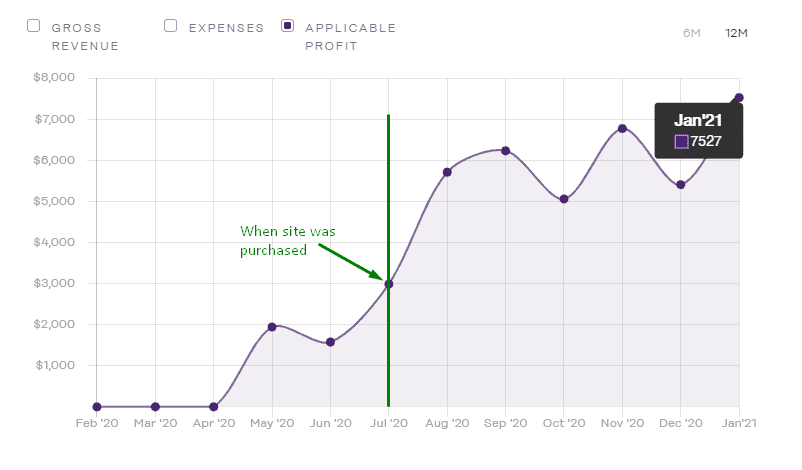

Underperforming websites, whilst a potential risk, can offer fantastic growth opportunities for investors. As an income-generating business, they can be optimized to make the most of the site’s performance which in turn has a knock-on effect on earnings and the overall valuation should you decide to sell.

Many people invest in fixer-upper websites in order to buy cheap, sell high once they’ve undergone the transformation process offering a real opportunity to grow your money.

Highly specific or trend-led niches run the risk of the topics a website targets falling out of favor and damaging (or eliminating) your income stream. Not every site can cover an evergreen topic so looking for ones with on-brand diversification opportunities should help in the event a keyword goes quiet.

Aside from perhaps property (and even that relies somewhat on market favorability), buying and selling websites offer investors the greatest control over their investment’s outcome.

With the ability to overhaul sites, optimize performance, boost traffic, diversify content and add new revenue streams you can make as much or as little money from the sites as you want.

Success with any investment isn’t guaranteed, and while a site might have page traffic and profits trending upwards that doesn’t mean it will continue when you take over. If you don’t have the technical expertise or the time required to run a site but still want to invest in websites, site management services like Buzz Logic could be a good option for you.

One of the biggest issues facing investors buying and selling websites is ending up with a scam site or fake buyer that could cost you thousands.

At Investors Club we verify listings before they go live and only work with vetted buyers to remove this risk and eliminate tire kickers.

As the new-kid-on-the-block investment type, we’re seeing increasing numbers of investors and even smaller Private Equity firms cashing in on the growing space. Compared to other more traditional investments, website investing offers easier and higher returns — typically between 30-60% annualized returns on growing sites.

With the added benefit of being able to hold multiple sites within your website investment portfolio, imagine the compounding effect of that MoM growth with 5 sites at your disposal?

Although not as illiquid as property, selling a website is not always a fast process. If you need access to money quickly, website investing risks tying up too much of your net worth.

The high brokerage fees for buying and selling sites, complex legal transfer process and site migration costs can also be a risk, eating into a large portion of your profits or available funds.

But not at Investors Club.

We put our members first and offer the lowest seller’s fees in the industry. To top it off we’ve eliminated buyer fees altogether and offer fee-free transfer, inspection, and escrow as standard giving our members more.

Analysis: Medium risk, ongoing high reward.

Final Thoughts

If you’re looking for excellent growth opportunities, passive income businesses, and don’t mind a little risk then website investing could be the perfect opportunity for you.

New businesses are added to our members-only marketplace every day. Your next investment is waiting.